(804) 353-4500tswinfo@tswinvest.com

You are leaving TSW

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

In recent weeks, The Wall Street Journal and The Financial Times published articles addressing the wide valuation and performance disparity between U.S. stocks and their foreign counterparts. Although they were published within days of each other, the articles reached opposing conclusions. While we find some agreement with both points of view, TSW takes a very different stance toward the perennial question “why own international stocks?”

On Thanksgiving Day, The Wall Street Journal published an attention-grabber titled “A Quarter of Your Retirement Fund Just Isn’t Keeping Up”1 by Ben Eisen that began “U.S. stocks have been euphoric lately—and they’ve left international stocks in the dust.” Eisen went on to document the outperformance of the S&P 500® Index over the past 15 years and suggested that many investors allocate far too many of their assets to “something that keeps falling behind.” He cited both an individual investor and a professional advisor who have thrown in the towel on international stocks completely, noting that large U.S. companies like McDonald’s and Microsoft “have significant foreign sales.” He added that investors have been pulling funds from international ETFs and mutual funds, offering the explanation that “the pain-to-benefit ratio isn’t worth it.”

A few days later Ruchir Sharma, chair of Rockefeller International, kept the shock factor high with his article, “The Mother of All Bubbles”2 published in The Financial Times. Sharma noted that the relative prices of U.S. stocks are “the highest since data began over a century ago and relative valuations are at a peak since data began half a century ago.” Warning that “a booming U.S. market is sucking money out of the others,” Sharma stated his opinion bluntly: “the U.S. is over-owned, overvalued and overhyped to a degree never seen before.”

TSW has no quarrel with The Wall Street Journal’s observation about the outperformance of U.S. stocks. That is just a fact. It is equally true that U.S. stocks are historically expensive relative to non-U.S. stocks. Both authors are right, but that’s where our agreement stops. TSW believes that the overwhelming reason to own international stocks in a well-rounded portfolio is that the world is dotted with great companies, many of which trade at attractive prices. This combination sets up the possibility of superior long-term returns. Like many of the best U.S. companies, these companies frequently have presence across global markets, including the U.S., and may dominate a particular market niche. Because of this, their country of domicile or the location of their stock listing is of little relevance to the investment case.

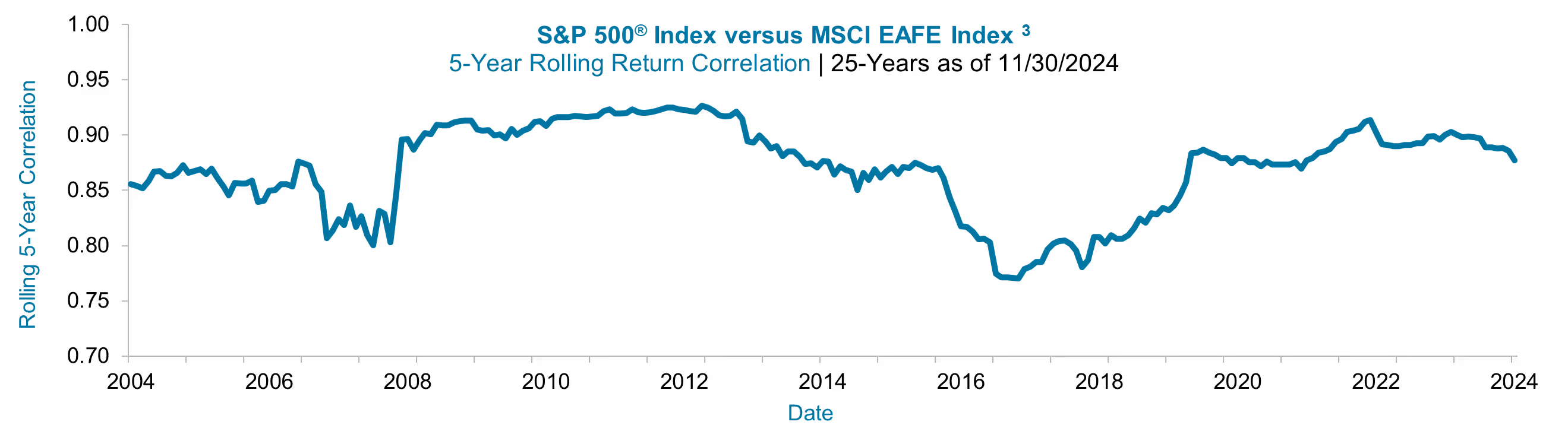

The Journal tiptoes around this point by noting that “one case for owning foreign stocks is that the rest of the world might do well when the U.S. is doing poorly.” TSW believes this isn’t very likely in today’s hyper-connected global economy. A set of circumstances leading the world’s largest economy to do poorly would likely have serious repercussions for other economies and investor sentiment alike. Except for brief dislocations, global stock market returns are highly correlated, as illustrated by the chart below. Both historical data and daily observation suggest that stocks mostly move together. These high correlations contradict the argument that U.S. stock returns will be persistently superior.

But wait a minute.

If global stocks really do march in unison, doesn’t this support the argument that one need only hold U.S. stocks to enjoy all the benefit? The answer is a resounding “no”. Constraining a portfolio to a single country excludes many attractive investment opportunities. Why would an investor consciously rule out great companies just because of geography, especially if those stocks are offered at appealing prices? Home country bias may be inevitable, but it isn’t an investment strategy.

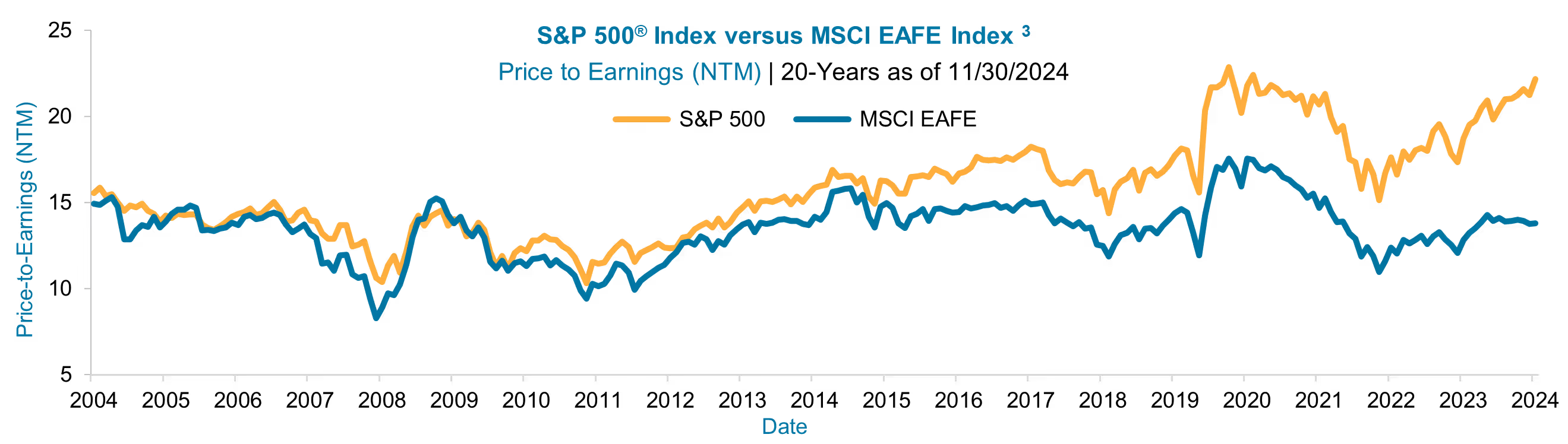

TSW also struggles with The Financial Times’ valuation point. We’ve seen the graphs. The price premium for U.S. stocks certainly looks extreme. But the U.S. market does enjoy some indisputable advantages: sophisticated financial markets, an entrepreneurial/risk-oriented culture, and a business-friendly legal structure (to name a few). Some premium is justifiable, although we can’t say what the right level is. By themselves, valuation measures, especially dogpile aggregations like “the price-to-earnings ratio of the S&P 500® Index versus international stocks”, are a lousy timing tool. The current U.S. premium could persist or go even higher. There are far too many unknowns to make a precise call. Likewise, the idea of reversion to a historical mean relationship between constantly changing and compositionally different stock indexes is a weak basis for investment decisions.

So why own international stocks? In our view, the answer is simple; there are great opportunities to earn attractive returns in companies based all around the world, and there’s no good reason for investors to shun those opportunities simply because of geography. Foreign stocks do present complexities such as politics and currency movements which can make them feel more risky and less certain, but this is where professionals like TSW have a role to play. TSW has invested in global stocks for more than three decades, and TSW believes the opportunities we see today are as good as ever.

The popular press will always try to make grand pronouncements about this or that. BusinessWeek magazine’s August 1979 cover story, “The Death of Equities”, might be the most famous example, but such declarations amount to little more than clickbait. The recent offerings from The Wall Street Journal and The Financial Times are no different. Read them for entertainment if you wish, but in our view, the best call is to stick with an allocation to both U.S. and international equities and ignore the facile arguments for lurching back and forth based on recent performance or dubious valuation comparisons.

1Eisen, Ben. “A Quarter of Your Retirement Fund Just Isn’t Keeping Up.” The Wall Street Journal. November 28, 2024. The article is publicly available at MSN.com.

2Sharma, Ruchir .‘The Mother of All Bubbles’ London Financial Times, December 2, 2024.

3Source: FactSet (December 2024).

Important Disclosure Information:

IMPORTANT DISCLOSURE: This commentary is intended for informational purposes only and does not constitute a complete description of our investment services, analysis, or performance. This commentary is in no way a solicitation or an offer to sell securities or investment advisory services. The expressed views and opinions contained herein are for informational purposes only, are based on current market conditions, and are subject to change without notice. Although information, opinions, and statistics contained herein have been obtained from sources believed to be reliable and are accurate to the best of our knowledge, Thompson, Siegel & Walmsley LLC (“TSW”) cannot and does not guarantee the accuracy, validity, timeliness, or completeness of such information and statistics made available to you for any particular purpose. This commentary should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Past performance is not indicative of future results. No part of this commentary may be reproduced in any form, distributed, or referred to in any other publication, without express written permission of TSW.

GENERAL ECONOMIC & MARKET COMMENTARY DISCLOSURE: Comments and general market related projections are based on information available at the time of writing and believed to be accurate; are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm and may not be relied upon for future investing. Certain information contained in this material represents or is based upon forward-looking statements, which can be identified by the use of terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of an Account may differ materially from those reflected or contemplated in such forward-looking statements. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results.

EQUITY SECURITIES RISK: Equity securities generally have greater risk of loss than debt securities. Stock markets are volatile, and the value of equity securities may go up or down, sometimes rapidly and unpredictably. The value of equity securities fluctuates based on real or perceived changes in a company’s financial condition, factors affecting a particular industry or industries, and overall market, economic and political conditions. If the market prices of the equity securities owned by the strategy fall, the value of your investment in the strategy will decline. Your portfolio may lose its entire investment in the equity securities of an issuer. A change in financial condition or other event affecting a single issuer may adversely impact securities markets as a whole.

INTERNATIONAL INVESTING RISK: Investments in global/international markets involve special risks not associated with U.S. markets, including greater economic, political and currency fluctuation risks, which are likely to be even higher in emerging markets. In addition, foreign countries are likely to have different accounting standards than those of the U.S.

PRINCIPAL RISK: Risk is inherent in all investing. Many factors and risks affect performance. The value of your investment, as well as the amount of return you receive on your investment, may fluctuate significantly day to day and over time. You may lose part or all of your investment in your portfolio or your investment may not perform as well as other similar investments. An investment in the strategy is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money if you invest in this strategy.

VALUE INVESTING RISK: The prices of securities TSW believes are undervalued may not appreciate as anticipated or may go down. The value approach to investing involves the risk that stocks may remain undervalued, undervaluation may become more severe, or perceived undervaluation may actually represent intrinsic value. Value stocks as a group may be out of favor and underperform the overall equity market for a long period of time, for example, while the market favors “growth” stocks.

Index Definitions:

S&P 500® Index: The index measures the performance of the large-cap segment of the market. Considered to be a proxy of the U.S. equity market, the index is composed of 500 constituent companies.

MSCI EAFE Index: The MSCI EAFE Index is an equity index which captures large and mid cap representation across 21 Developed Markets countries around the world, excluding the U.S. and Canada. The Index covers approximately 85% of the free float adjusted market capitalization in each country.

Subscribe to receive the latest news and updates

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.