(804) 353-4500tswinfo@tswinvest.com

You are leaving TSW

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

In TSW’s more than 20-year history of investing in domestic value equities with our current portfolio management team, we have not felt any obligation to describe the seemingly nuanced “flavors of value”, and ultimately where we fit into the mix. This is particularly interesting given the majority of our current U.S. equity team’s existence has been in a prolonged growth cycle. However, the need to be explicit in describing flavors of value, particularly in context to the domestic market environment, has changed over the last handful of years given the market backdrop that witnessed one of the largest valuation gaps in history between the most expensive U.S. stocks and its cheaper cohorts. Specifically, this became notably acute during what we have deemed to be the last few years of the growth cycle ending or peaking in the first quarter of 2021. During this period, we noticed a high correlation of top performing U.S. equity managers exhibiting very lofty valuation multiples, often surpassing even core indices. Not dissimilar from other cycle peaks, style drift was also a general observation for some value managers.

Quite simply, while U.S. equity markets have shifted modestly in value’s favor since this time, we continue to live in one of the largest historical disconnects between value and growth, and coincidentally one of the largest valuation gaps between the most expensive and cheapest names in the broad market. When looking in the rearview mirror at different points of time over the last handful of years, managers who by nature have less price sensitivity (i.e., more expensive valuation multiples than their respective value index) have arguably had the winds at their back, while those that are more price sensitive have had the winds in their face. This is an important concept – false conclusions around “skill” or lack thereof can be drawn in such heightened historical periods of dislocation in a cycle. Equally as important, as one looks prospectively, those same structural biases inevitably can become notable tailwinds (for price sensitive managers with a true value bias), or headwinds for the opposing posture. Given this backdrop, we ultimately believe it is more imperative than ever for U.S. equity investors to understand their manager’s process, style, and performance expectations in context to the cycle we live in.

At TSW, consistency is the hallmark of our investment process. The process is disciplined and repeatable, and we apply it to every stock we analyze for every equity portfolio we manage, regardless of what’s going on in the market. We understand our value fit within the context of a client’s aggregate portfolio, and do not allow irrational exuberance or market favoritism to shift our focus from our stated mandate.

Below, we describe what we believe to be the styles of value we are most often competing against in the U.S. equity market, acknowledging the generalizations stated below.

Deep Value: This approach to value seeks to identify securities that are considered extremely undervalued or in distress. Within this type of value investing, cheapness (commonly assessed on a price to book basis), is often the most dominant overarching factor and driver when assessing securities. Many of these strategies have tended to do well in markets embracing heightened risk given their typical higher beta posture, as well as when the value factor is being rewarded. Conversely, down-markets or those where the value factor is disregarded or penalized have tended to be more challenging. Unfortunately, when the value factor is out of vogue, the challenged results can be significant given the prominence given to the factor.

Traditional Value: Traditional value typically involves rigorous fundamental analysis to find stocks that are undervalued relative to their intrinsic value. This stylistic approach is price sensitive in nature, often incorporating a principle of investing called margin of safety which describes a situation where a security’s market price trades significantly below the supposed intrinsic value. While directionally similar to deep value in the sense of having explicit exposure to the value factor (i.e., typically comprising a valuation discount to the index), these strategies may not have as polarizing of returns given other offsetting factors such as the margin of safety lens and other fundamental considerations. Traditional value is how we at TSW define ourselves when referring to our domestic strategies. We ultimately seek to identify stocks that trade at a discount to intrinsic value, with identifiable catalysts we believe will likely come to fruition over our holding period, thereby unlocking value.

Relative Value: We consider relative value investing to be general approaches that are typically less price sensitive than both deep value and traditional value. The style could often be associated with taking the valuations of other comparable businesses into consideration as a primary means for analyzing a security’s relative attractiveness as opposed to assessing a margin of safety relative to an intrinsic value. Other approaches to this style often get grouped with the subjective notion of “quality”, whereby attractiveness may be considered in context to such attributes as recurring revenue, clean balance sheet, high return on equity, among others. While these are all great attributes to have, in our view they should be considered in context to valuation and risk/reward, key components that we look for from our domestic team’s traditional value lens. Ultimately, we would argue the relative value posture is where a significant number of managers currently reside within domestic value equities. Given most relative value strategies trade at a premium valuation multiple relative to the associated value benchmark, this posture has been at times a stylistic tailwind for many peers given the prolonged growth rotation favoring more expensive names in U.S. markets.

Growth at a Reasonable Price (“GARP”): GARP is the most growth-oriented style of the prior three that we have described, although still within the value style. This style is the least price sensitive metric, and is arguably looking around the corner for growth extrapolation in relation to a company’s current valuation. Managers of GARP strategies prioritize companies that display strong and consistent earnings growth above standard market levels and/or historical company levels, while excluding those with cheaper valuations. The primary aim is to avoid the extremes associated with both growth and value investing, but not surprisingly often tends to look more “core-like” than value.

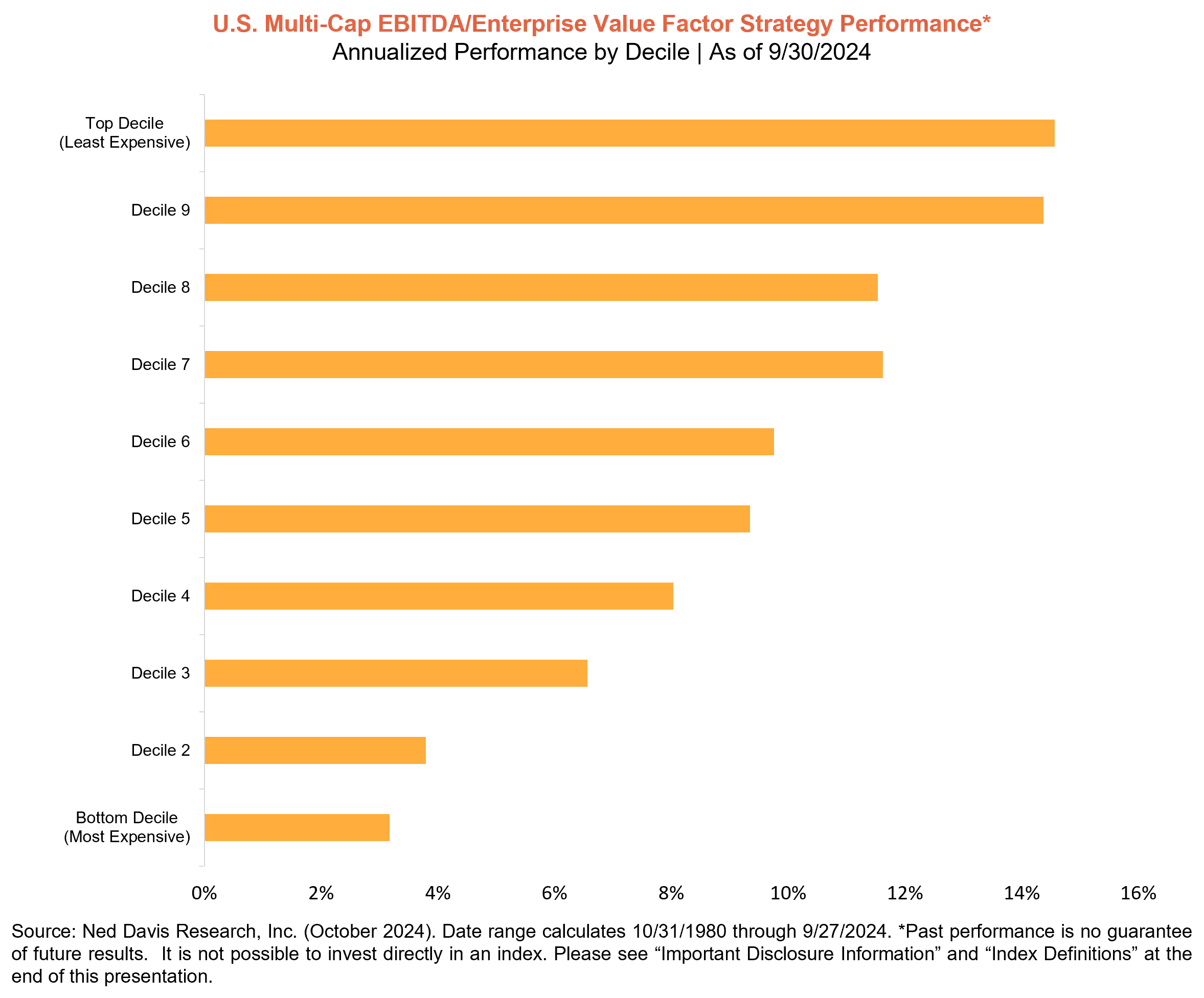

Despite the current cycle described and the end point sensitivity associated, the value factor has proven to be an important driver of alpha generation in U.S. markets. As shown below, since 1980 (first available data for the factor we could access), the cheapest decile of EV/EBITDA as a factor has outperformed the most expensive decile by over 11% on an annualized basis for more than 44 years (Ned Davis Research). As one can see, the relationship is quite linear with more expensive stocks underperforming their cheaper counterparts.

There are clearly advantages and disadvantages to each style of value described. However, given the prolonged outperformance of growth compared to value and the inevitable occurrence of style drift, allocators need to be certain that their managers are truly “value” managers. Specifically, we believe that when the value factor begins to work in a more sustainable way as it has historically, we would expect it to be a greater stylistic tailwind for TSW’s domestic strategies and other traditional value managers. As stated, we believe the set-up today continues to provide one of the most compelling periods in time to think about value and the related sub-styles described above.

IMPORTANT DISCLOSURE: This commentary is intended for informational purposes only and does not constitute a complete description of our investment services, analysis, or performance. This commentary is in no way a solicitation or an offer to sell securities or investment advisory services. The expressed views and opinions contained herein are for informational purposes only, are based on current market conditions, and are subject to change without notice. Although information, opinions, and statistics contained herein have been obtained from sources believed to be reliable and are accurate to the best of our knowledge, Thompson, Siegel & Walmsley LLC (“TSW”) cannot and does not guarantee the accuracy, validity, timeliness, or completeness of such information and statistics made available to you for any particular purpose. This commentary should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Past performance is not indicative of future results. No part of this commentary may be reproduced in any form, distributed, or referred to in any other publication, without express written permission of TSW.

GENERAL ECONOMIC & MARKET COMMENTARY DISCLOSURE: Comments and general market related projections are based on information available at the time of writing and believed to be accurate; are for informational purposes only, are not intended as individual or specific advice, may not represent the opinions of the entire firm and may not be relied upon for future investing. Certain information contained in this material represents or is based upon forward-looking statements, which can be identified by the use of terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “target”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of an Account may differ materially from those reflected or contemplated in such forward-looking statements. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decisions. Past performance is not indicative of future results.

EQUITY SECURITIES RISK: Equity securities generally have greater risk of loss than debt securities. Stock markets are volatile, and the value of equity securities may go up or down, sometimes rapidly and unpredictably. The value of equity securities fluctuates based on real or perceived changes in a company’s financial condition, factors affecting a particular industry or industries, and overall market, economic and political conditions. If the market prices of the equity securities owned by the strategy fall, the value of your investment in the strategy will decline. Your portfolio may lose its entire investment in the equity securities of an issuer. A change in financial condition or other event affecting a single issuer may adversely impact securities markets as a whole.

PRINCIPAL RISK: Risk is inherent in all investing. Many factors and risks affect performance. The value of your investment, as well as the amount of return you receive on your investment, may fluctuate significantly day to day and over time. You may lose part or all of your investment in your portfolio or your investment may not perform as well as other similar investments. An investment in the strategy is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You may lose money if you invest in this strategy.

VALUE INVESTING RISK: The prices of securities TSW believes are undervalued may not appreciate as anticipated or may go down. The value approach to investing involves the risk that stocks may remain undervalued, undervaluation may become more severe, or perceived undervaluation may actually represent intrinsic value. Value stocks as a group may be out of favor and underperform the overall equity market for a long period of time, for example, while the market favors “growth” stocks.

For additional information regarding potential risks to your investment please see risk disclosures in our Form ADV Part 2A found here https://www.tswinvest.com.

©2024 Thompson, Siegel & Walmsley LLC (“TSW”). TSW is an investment adviser registered with the SEC. Registration does not imply a certain level of skill or training. All information contained herein is believed to be correct but accuracy cannot be guaranteed. TSW and its employees do not provide tax or legal advice. TSW is a trademark in the United States Patent and Trademark Office.

Subscribe to receive the latest news and updates

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.

You are now leaving the TSW website. This link is provided as a convenience, and Thompson, Siegel & Walmsley is not responsible for the content provided on your destination site.